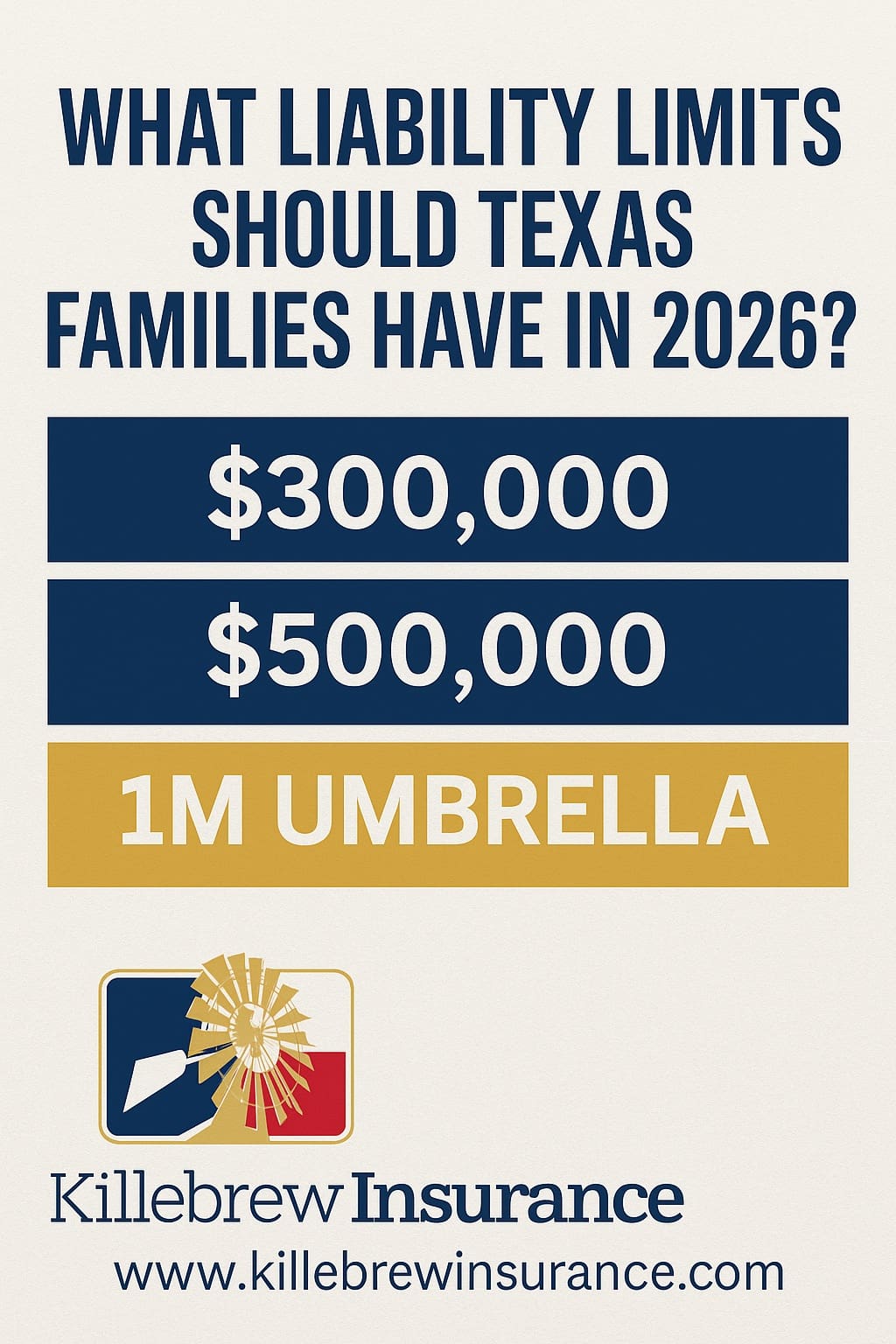

Liability claims are rising across Texas, and many homeowners still carry outdated limits like $100,000 — which is not enough in 2026. Families in Midland, Odessa, Big Spring, Andrews, Monahans, Lubbock, and Amarillo should consider increasing liability to $300,000, $500,000, or adding a $1M umbrella for stronger financial protection. Killebrew Insurance LLC helps West Texas homeowners get the right liability coverage for real-life risks.

Call Odessa: 432-332-6322, Midland: 432-694-0508, or visit www.killebrewinsurance.com.

- Liability claims have increased sharply in Texas due to medical costs and lawsuits.

- $100,000 liability is now considered insufficient for most families.

- Recommended 2026 limits: $300,000, $500,000, or $1M umbrella.

- Common liability claims include dog bites, slip-and-fall injuries, tree damage, and accidents involving guests or contractors.

- This guide is for responsible homeowners, not price-only shoppers.

⚖ Why Liability Limits Matter More in 2026

Many homeowners focus on property damage and roof coverage — but liability claims can be far more expensive.

In Texas, liability claims include:

- Injuries on your property

- Dog bites

- Fallen tree damage

- Accidents involving contractors

- Lawsuits from guests

- Damage caused by children or pets

- Pool-related injuries

- Fire damage that spreads to another home

Medical costs and legal fees have risen significantly since 2020, and jury settlements are increasing across the state.

This makes upgrading liability limits in 2026 critical for protecting your financial future.

???? What Liability Limits Do Texas Homeowners Commonly Carry?

Most older policies still show:

❌ $100,000 Liability Limit

This was acceptable 15–20 years ago, but no longer protects against modern claim costs.

⭐ Recommended in 2026

Based on current claim trends in Texas:

- $300,000 — Good

- $500,000 — Better

- $1,000,000 (Umbrella) — Best

These limits better align with real-world risks and current medical/legal expenses.

???? Texas Liability Trends: Why Costs Are Rising

According to data from the Insurance Information Institute and NAIC:

✔ Medical expenses continue to outpace inflation

✔ Attorney fees and court costs are rising

✔ Jury settlements are larger in 2026

✔ More claims involve multiple parties

✔ Property damage often affects neighbors too

This means a single incident can easily exceed $100,000.

???? Common Liability Claims in West Texas (Real Examples)

• Tree falls onto a neighbor’s home

A windstorm knocks down a homeowner’s dead tree → causes $40,000 damage.

• Guest slips on stairs and breaks an ankle

Medical bills + PT + lost wages → often exceed $75,000.

• Dog bite injuries

Can result in $20,000–$150,000 depending on medical treatment.

• Child damages another homeowner’s property

Fence, windows, vehicles → liability covers these.

• Pool or trampoline injuries

Claims are more frequent and more expensive in 2026.

All of these are scenarios where $100,000 is not enough.

???? Why a $1M Umbrella Policy Is Becoming More Popular

An umbrella is one of the most cost-effective protections for West Texas families.

It provides:

- Additional $1M+ liability protection

- Coverage above both home and auto liability

- Protection against lawsuits

- Security for your savings and future income

For many families, umbrellas cost $20–$35 per month, depending on carrier.

???? How to Choose the Right Liability Limit in 2026

Ask yourself:

✔ If someone sued me tomorrow, what assets need protection?

✔ Would $100,000 cover a major injury?

✔ Do I have a pool, trampoline, pets, or frequent visitors?

✔ Is my home valued above $300,000?

✔ Do I want to protect my income and savings?

If any answer is “yes,” your liability limit should be $300,000–$500,000 minimum, or an umbrella.

❓ FAQ: Liability Coverage Questions in 2026

1. Is $100,000 liability still acceptable?

Not anymore — costs regularly exceed this.

2. Does increasing liability increase my premium a lot?

Usually very little — often less than $5–$12/mo.

3. Do I need an umbrella?

If you have assets, a pool, pets, or children — umbrellas are strongly recommended.

4. Does liability cover damage to my own property?

No — it covers damage or injuries you cause to others.

5. Does bundling help with liability pricing?

Yes — bundling can reduce the cost of higher liability and umbrellas.

???? Protect Your Financial Future With the Right Liability Limits

We help West Texas families choose the right liability limits for real-world risks.

???? Odessa: 432-332-6322

???? Midland: 432-694-0508

???? www.killebrewinsurance.com

Serving families in Midland, Odessa, Monahans, Andrews, Big Spring, Lubbock, Amarillo, and surrounding areas.

???? Author Bio

Craig Killebrew, agency manager at Killebrew Insurance LLC, has over 20 years of experience protecting West Texas families with smart coverage strategies and personalized risk planning.

???? Sources

- Insurance Information Institute (III)

- NAIC Consumer Reports

- Texas Department of Insurance (TDI)

- CDC Injury Cost Database