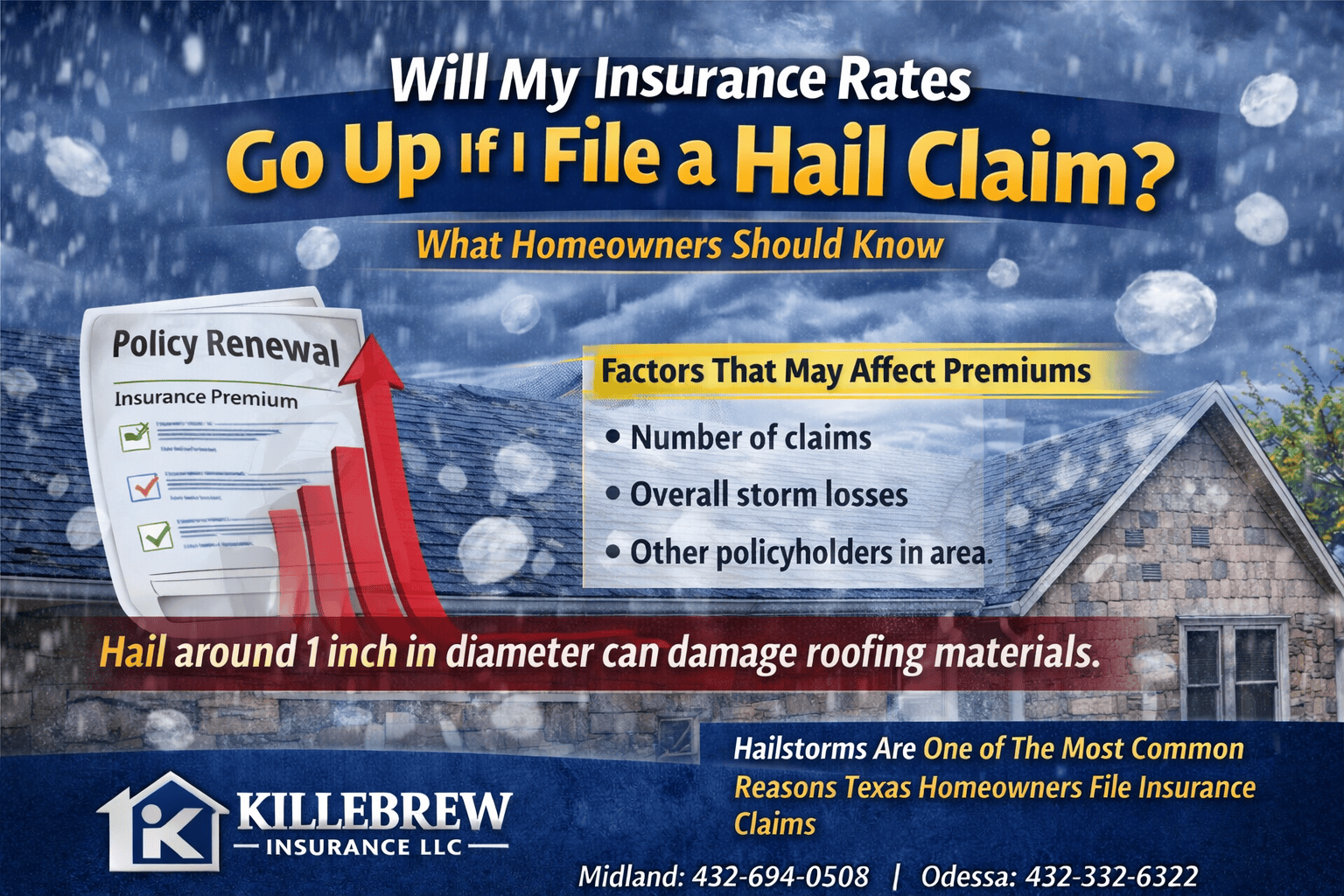

What Homeowners Should Know

After a hailstorm damages a home, many homeowners wonder whether filing an insurance claim could cause their premiums to increase.

The answer can depend on several factors including the type of claim, the number of claims filed, and regional storm activity.

Short Answer

A hail claim may affect insurance premiums in some situations, but the impact can vary depending on the insurance company, the homeowner’s claim history, and broader storm trends in the region.

Factors That May Influence Insurance Rates

Insurance companies often consider several factors when reviewing policy renewals.

These may include:

-

number of claims filed

-

type of claim

-

overall storm losses in the area

-

underwriting guidelines

-

changes in construction costs

In regions that experience frequent storms, premium adjustments may sometimes occur across a larger group of policies rather than being tied to a single claim.

Catastrophe Claims vs Other Claims

Hailstorms are often classified as catastrophe events when they affect large areas.

In these cases, insurance companies may evaluate risk across an entire region rather than focusing on one individual policy.

However, policies and underwriting practices can vary.

When Homeowners Often File a Claim

Homeowners commonly file a claim when:

-

roof damage is extensive

-

repair costs exceed the deductible

-

structural damage occurs

-

leaks or interior damage are present

A roof inspection can help determine the extent of storm damage.

Why Hail Claims Are Common in West Texas

Storm systems across Midland, Odessa, and surrounding West Texas communities frequently produce hail and strong winds.

Because of this weather pattern, hail damage is one of the most common reasons homeowners file insurance claims in the region.

What Experts Say

The Insurance Institute for Business and Home Safety reports that hailstorms are a leading cause of property damage across the United States.

Consumer guidance from the Texas Department of Insurance also recommends reviewing your policy and deductible to understand how storm damage claims may apply.

Important Note

Because insurance policies, coverages, and deductibles can vary by carrier and endorsements, homeowners should review their individual policy or speak with a licensed insurance professional to understand their specific coverage.

???? Midland Office: 432-694-0508

???? Odessa Office: 432-332-6322

???? www.killebrewinsurance.com