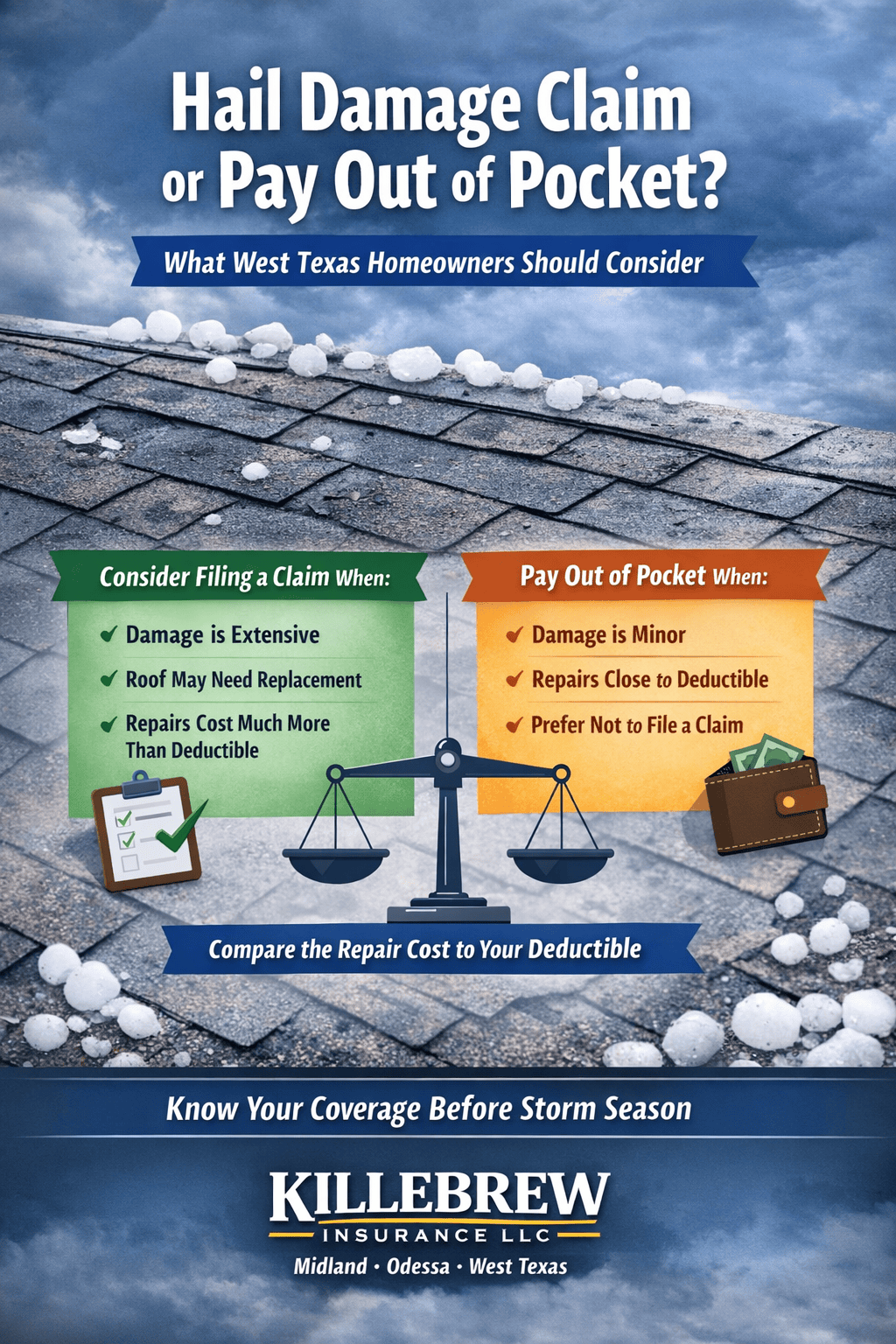

What West Texas Homeowners Should Know

After a hailstorm hits Midland, Odessa, or surrounding West Texas communities, many homeowners are faced with an important question:

Should a claim be filed, or should repairs be handled out of pocket?

The answer can depend on several factors, including the amount of damage, deductible, and estimated repair cost.

Short Answer

Many homeowners compare the estimated repair cost to their deductible when deciding whether to file a claim.

If the repair cost is significantly higher than the deductible, some homeowners consider filing a claim. If the cost is close to the deductible, others may choose to pay for repairs out of pocket.

Example

Repair Cost Deductible Potential Insurance Payment

Repair cost Deductible Potential Ins Payment

$10,000 $5,000 $5,000

$6,000 $5,000 $1,000

When the difference between the repair cost and deductible is smaller, some homeowners decide not to file a claim.

Factors Homeowners Often Consider

When evaluating their options after a storm, homeowners may consider:

-

deductible amount

-

repair estimate

-

roof condition

-

claim history

-

insurance company guidelines

Each situation can vary depending on the policy and the extent of the damage.

Situations Where Homeowners Often Consider Filing a Claim

Some homeowners consider filing a claim when:

-

damage appears extensive

-

the roof may require replacement

-

repair costs are significantly higher than the deductible

-

interior damage or leaks are present

Situations Where Homeowners Sometimes Pay Out of Pocket

In other situations, some homeowners choose to handle repairs themselves when:

-

damage appears minor

-

repair costs are close to the deductible

-

they prefer not to file a claim

Why Timing Matters

It is important not to wait too long if damage is suspected.

Some insurance policies include time limits for reporting storm damage, and certain carriers may require claims to be reported within a specific time period after the date of loss.

Because requirements can vary by policy, homeowners often choose to have the roof inspected after a significant storm to determine whether damage may be present.

Why This Matters in West Texas

Severe storms frequently affect Midland, Odessa, and surrounding West Texas areas, bringing hail and strong winds that can damage roofs.

Because of this, homeowners in this region often face decisions about whether to file a claim after storm events.

Understanding how deductibles and coverage may apply can help homeowners feel more prepared after a storm.

What Experts Say

Research from the Insurance Institute for Business and Home Safety shows that hailstorms are a leading cause of roof damage in many parts of the United States.

Consumer guidance from the Texas Department of Insurance encourages homeowners to review their policies and understand their deductible before filing a claim.

Educational resources from the Insurance Information Institute explain that claim decisions often depend on the extent of damage and the specific terms of the policy.

Important Note

Because insurance policies, coverages, and deductibles can vary by carrier and endorsements, homeowners should review their individual policy or speak with a licensed insurance professional to understand their specific coverage.

About Killebrew Insurance LLC

This article was prepared by the team at Killebrew Insurance LLC, an independent insurance agency serving Midland, Odessa, and communities across West Texas.

Our team helps homeowners better understand their coverage and review their insurance options.

Questions About Your Coverage?

Killebrew Insurance LLC

Midland Office: 432-694-0508

Odessa Office: 432-332-6322

???? www.killebrewinsurance.com

Disclaimer

The information in this article is provided for general educational purposes only and is not intended to provide specific insurance advice. Coverage may vary by policy, carrier, endorsements, and individual circumstances. Please review your policy and speak with a licensed insurance professional to understand your specific coverage.